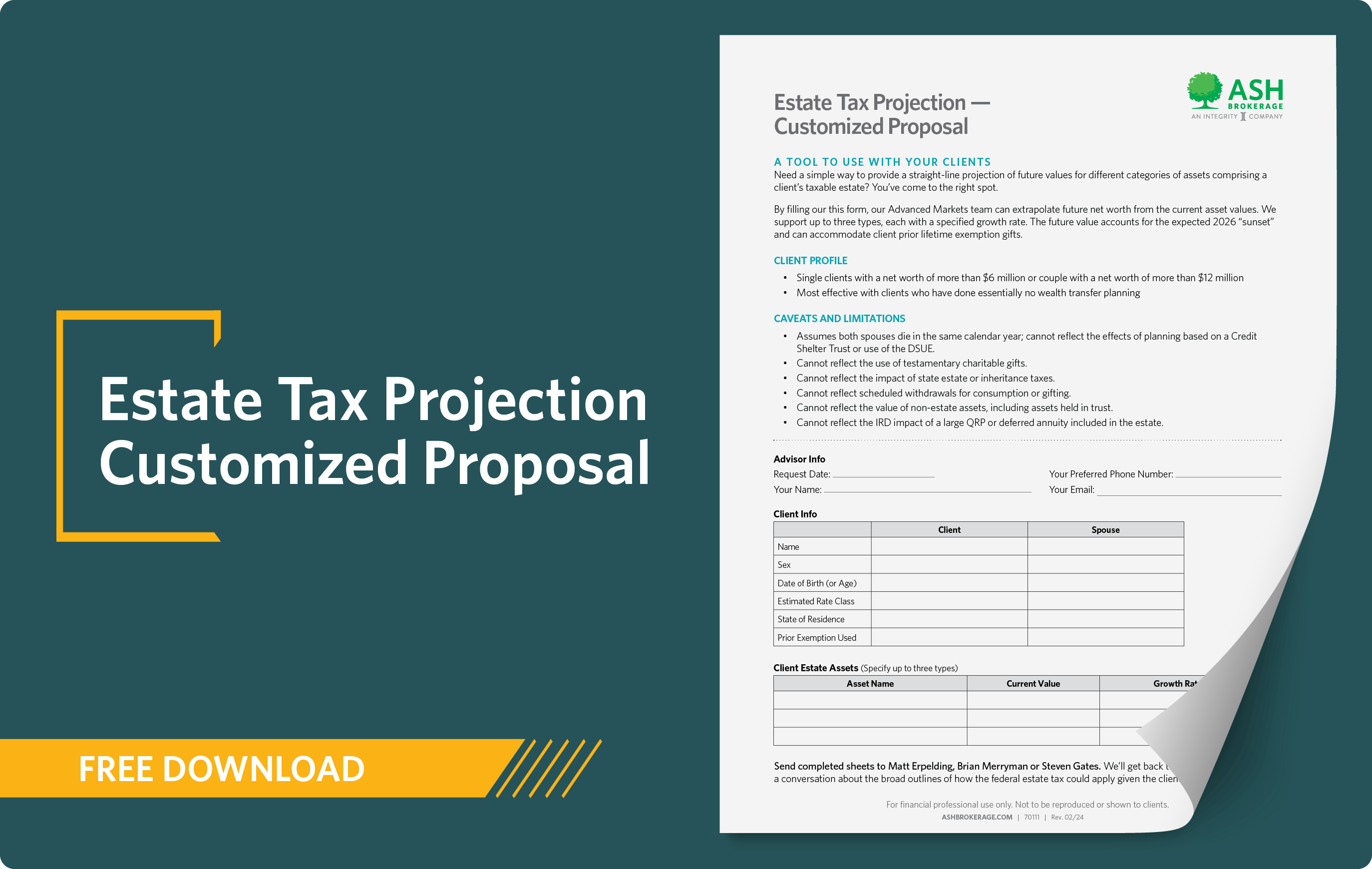

Estate Tax Planning: Considering State Taxes Can Benefit Your Clients

The Story

You’re probably aware of the federal state tax exemption sunsetting on Dec. 31, 2025. But did you know that many states also have state estate taxes? There’s no sunsetting for state taxes—so there’s nothing in the future to wait for. Clients living in states with state estate taxes can experience immediate benefits by planning now.

Client Profile

David and Mary, both age 65, live in Washington, a state with a maximum state estate tax of 20%. With assets of $10M, they aren’t affected by the sunsetting of the federal exemptions and hadn’t really considered estate planning to be a big priority until their financial advisor brought it up.

If the estate grows at a rate of 4% each year, here’s a hypothetical projection of how David and Mary’s estate could look upon their deaths:

The Strategy

David and Mary have four options available to choose from when it comes to paying their estate taxes.

- Cash: Pay $5,018,137 out of pocket

- Sale of assets: Assuming a sale at 80% of market value, the cost would be $6,272,671

- Take a loan: A 10-year loan with a 7% interest rate would cost $7,144,698

- Life insurance: An SUL with a $5M death benefit would cost $2,012,742 (assuming an annual premium of $74,546 paid for 27 years)

Results

David and Mary chose option four, both qualifying for preferred non-tobacco rates. By leveraging life insurance, they plan to use their tax-free death benefit to pay the estate taxes — increasing their wealth transfer to their heirs by more than $3M.

If you have clients in states with state estate taxes, don’t wait. Get started now by downloading our fact finder.

Through analytical expertise, Steven Gates supports advisors serving high-net-worth clients and business owners. Using customized modeling, he creates insurance-driven strategies for wealth transfer, business protection and charitable leverage. Steven is the go-to guy when you need a unique blend of technological expertise, industry knowledge and entrepreneurial drive.